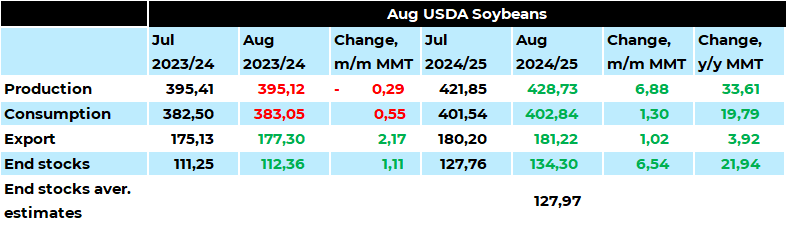

Серпневий WASDE збільшив прогноз світового урожай сої

у 2024/25 МР на 6,9 млн тонн до 428,7 млн тонн. Урожай у США збільшено на

4,2 млн тонн до 124,9 млн тонн завдяки більшій площі та врожайності, що

перевищило очікування ринку. Урожай в Україні зріс на 1,3 млн тонн до

рекордних 6,8 млн тонн, оскільки площа збирання була підвищена на 0,7 млн га - до історичного максимуму в

2,9 млн га, що більше за 2,6 млн га за офіційною

оцінкою Укрстату. Крім того, прогноз WASDE щодо врожайності сої в Україні досить оптимістичний - на рівні 2,35 т/га, незважаючи на спекотне літо.

російський урожай збільшився на 0,7 млн тонн до 7,3 млн тонн. Урожай в Індії

збільшився на 0,6 млн тонн до 12,8 млн. тонн.

Глобальний експорт у 2024/25 МР підвищено на 1 млн тонн до 181,2 млн тонн. Прогноз для США було збільшено на 0,7 млн тонн до

50,4 млн тонн «через збільшення пропозиції при стабільній переробці». Для України

експорт зріс на 0,8 млн тонн до 4,3 млн тонн через вищій врожай. російський

експорт зріс на 0,4 млн тонн до 1,3 млн тонн. У свою чергу, експорт Аргентини

на наступний сезон скорочено на 1 млн тонн до 4,5 млн тонн.

Світове споживання сої підвищено на 1,3 млн тонн до 402,8 млн. тонн.

Кінцеві світові запаси у 2024/25 МР істотно

підвищено - на 6,5 млн тонн до 134,3 млн тонн «головним чином завдяки вищим

запасам у Китаї, США та Аргентині, які частково компенсували зниження запасів у

Бразилії». Це значно вище очікуваних 128 млн тонн. Запаси США були переглянуті

вгору на 3,4 млн тонн до 15,3 млн тонн, що набагато вище, ніж очікувалося.

Щодо 2023/24 МР, то оцінку врожаю в Аргентині скорочено на 0,5 млн тонн до 49 млн тонн.

Експорт із Бразилії у 2023/24 МР підвищено на 2

млн тонн до 105 млн тонн «на основі високих темпів поставок». Прогноз імпорту до Китаю зріс на 3,5 млн тонн до 11,5 млн тонн «за рахунок збільшення поставок з боку експортерів».

Щодо ріпаку, світове виробництво в

2024/25 МР було підвищено на 0,9 млн тонн до 88,8 млн тонн «переважно через вищі площі для росії», що підштовхнуло російський урожай на 0,8 млн тонн м/м до 5,1 млн тонн.

Глобальний експорт ріпаку у 2024/25 МР підвищено на 0,2 млн тонн до 17,5 млн тонн, лише з невеликим переглядом у бік зростання

для росії – на 175 тис. тонн до 925 тис. тонн. Прогноз українського експорту

залишено без змін на рівні 3,3 млн тонн, а переробка очікується на рівні 400

тис. тонн.

Серед імпортерів єдина зміна відбулася для Китаю – підвищення на 200 тис. тонн до 3,9 млн. тонн.

Пов'язані продукти

Прокоментувати