Надлишкова пропозиція залишається ключовою

темою на світовому ринку пшениці: вересневий звіт WASDE від USDA підтвердив

рекордно високий урожай і зростання експортних надлишків, що продовжує тиснути

на ціни.

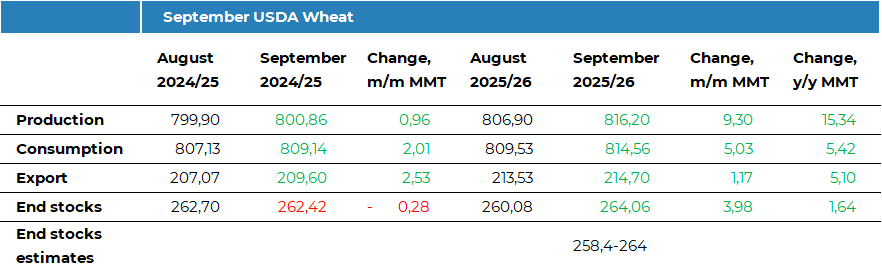

Світове виробництво пшениці у 2025/26 МР

підвищене на 9,3 млн т — до нового рекорду 816,2 млн т. Найбільші коригування

вгору зафіксовані в Австралії (+3,5 млн т до 34,5 млн т завдяки сприятливим

умовам), ЄС (+1,85 млн т до 140,1 млн т на основі результатів жнив), та росії

(+1,5 млн т до 85 млн т, що все ж нижче за локальні оцінки близько 87 млн т). Прогнози

для України та Канади підвищені на 1 млн т для кожної — до 36 млн т та 23 млн т

відповідно, тоді як Казахстан додав 0,5 млн т до 16 млн т.

Світовий експорт було переглянуто лише

незначно вгору — на 1,2 млн т до 214,7 млн т. Прогноз для Австралії зріс на 2

млн т до 25 млн т, тоді як для США — на 0,7 млн т до 24,5 млн т, що відображає

стабільний попит на пшеницю HRW та активні відвантаження.

На тлі різкого підвищення виробництва й

обмежених змін у торгівлі та споживанні, світові кінцеві запаси тепер

оцінюються у 264,1 млн т — майже на 4 млн т більше, ніж у серпні, і вище за

очікування ринку, головним чином через зростання у ключових

країнах-експортерах. Натомість у США кінцеві запаси скорочені на 0,7 млн т — до

23 млн т, що трохи нижче, ніж торік, і нижче за середні оцінки трейдерів.

Загалом, звіт створив додатковий тиск на ринок пшениці. На тлі зростання виробництва та запасів світова пропозиція залишається важкою, і цей фактор, імовірно, й надалі тиснутиме на ціни у короткостроковій перспективі.

Детальний

огляд інших культур доступний для передплатників ASAP Agri Premium: https://asapagri.com/products/premium.

Прокоментувати