У червневому звіті WASDE прогноз світового

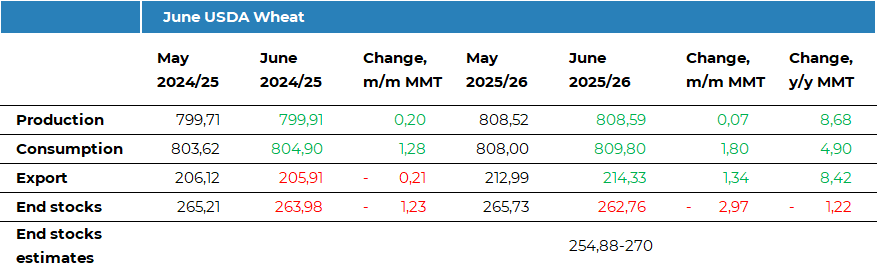

виробництва пшениці на 2025/26 МР залишено практично без змін — 808,6 млн тонн,

що є рекордним рівнем і посилює очікування надлишкової пропозиції. Прогноз для ЄС

підвищено на 0,6 млн тонн — до 136,6 млн тонн завдяки покращенню стану посівів

в Іспанії, а для Індії — на 0,5 млн тонн — до 117,5 млн тонн.

Світовий експорт пшениці у 2025/26 МР

переглянуто в бік зростання на 1,3 млн тонн — до 214,3 млн тонн. Прогноз експорту

США підвищено на 0,7 млн тонн — до 22,5 млн тонн завдяки активним продажам на

початку сезону, а ЄС — на 0,5 млн тонн — до 34,5 млн тонн.

Кінцеві світові запаси пшениці на 2025/26 МР

прогнозуються на рівні 262,8 млн тонн, що на 3 млн тонн менше порівняно з

попереднім місяцем і нижче за середній ринковий прогноз. В США запаси

очікуються на рівні 24,5 млн тонн, що на 0,7 млн тонн менше м/м через вищий

експорт. Хоча це й нижче очікувань ринку, показник все ще на 7% вищий у річному

вимірі.

Щодо поточного сезону 2024/25, глобальні

кінцеві запаси знижено на 1,2 млн тонн — до 263,9 млн тонн, переважно через

перегляд у бік зниження для росії. Тим часом, прогноз імпорту пшениці Китаєм у

2024/25 МР підвищено на 0,7 млн тонн — до 4 млн тонн.

У

підсумку звіт не приніс суттєвих сюрпризів. Попри тиск із боку рекордної

глобальної пропозиції, зниження світових і американських запасів у поєднанні зі

зростанням експорту з США частково стримують «ведмежий» тиск на ціни.

Детальний

огляд інших культур доступний для передплатників ASAP Agri Premium: https://asapagri.com/products/premium.

Пов'язані продукти

Прокоментувати