Звільнення українського аграрного експорту від тарифів і квот, яке Європейський Союз запровадив у 2022 році після повномасштабного вторгнення Росії, має завершитися 5 червня 2025 року. Хоча ці заходи — так звані Автономні торговельні преференції (АТП) — вже неодноразово подовжувалися, цього разу Брюссель може відновити тарифи на окремі продукти.

Поки Україна та ЄС працюють над компромісним варіантом «вільної торгівлі» для агропродукції, головний зерновий аналітик ASAP Agri Інна Степаненко аналізує, як змінювався експорт українського зерна в умовах АТП — і що може статися, якщо тарифи та квоти повернуться.

Що було до АТП: режим торгівлі до лібералізації

До повної лібералізації експорту в межах АТП, ЄС застосовував тарифні квоти (TRQ) для українського зерна. У 2021 році безмитні річні квоти становили:

- пшениця — 1 млн тонн

- кукурудза — 650 тис. тонн

- ячмінь — 350 тис. тонн

У разі перевищення квоти застосовувалися тарифи за режимом найбільшого сприяння (MFN):

- пшениця — 95 EUR/т

- ячмінь — 93 EUR/т

- кукурудза — 94 EUR/т

Втім, для кукурудзи змінна тарифна система ЄС у той період часто означала нульові або мінімальні мита завдяки високим світовим цінам.

Сплеск експорту українського зерна до ЄС

Повна лібералізація торгівлі з ЄС суттєво збільшила експорт українського зерна до країн блоку.

У 2020/21 МР частка ЄС у експорті української пшениці становила лише 4% (близько 0,7 млн тонн). У 2023/24 МР вона зросла до 46% (8,5 млн тонн).

Іспанія стала провідним ринком

ЄС для української пшениці й загалом найбільшим її імпортером у світі у 2023/24

МР. Попри зниження обсягів у 2024/25 МР, Іспанія залишається ключовим

напрямком, а Італія демонструє помітне зростання попиту.

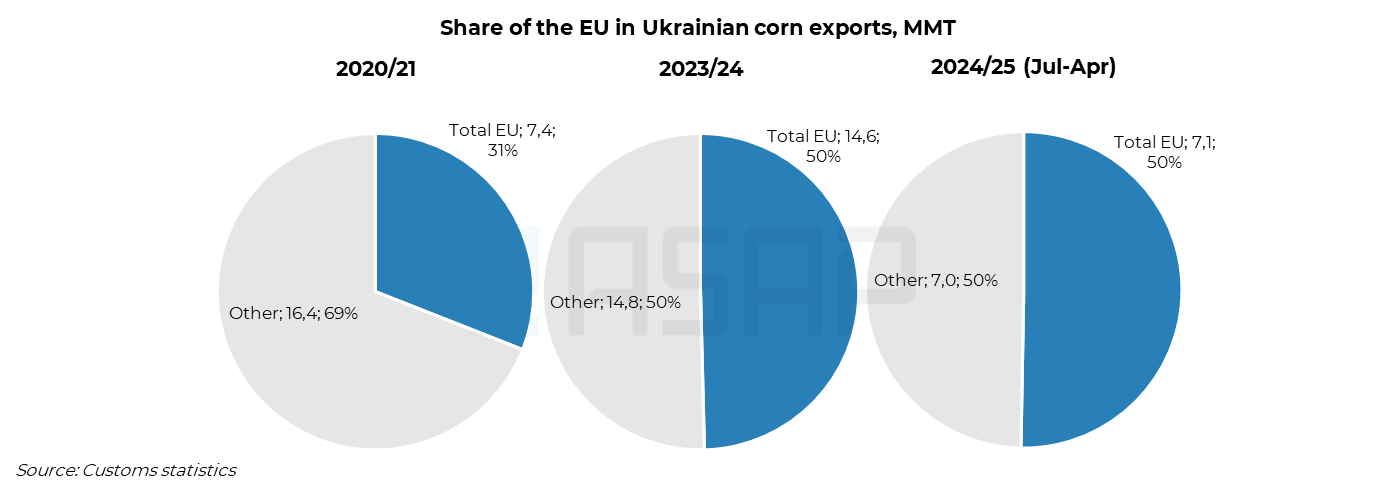

Кукурудза й раніше була важливою позицією в експорті до ЄС. У 2020/21 МР Євросоюз імпортував 7,4 млн тонн кукурудзи з України, що становило 31% загального експорту. Завдяки АТП частка ЄС у 2023/24 МР зросла до 50% (14,6 млн тонн).

І знову Іспанія була попереду —

не лише як найбільший покупець з ЄС, але й як основний напрямок української

кукурудзи у світі. Також спостерігалося значне зростання експорту до Італії,

тоді як Нідерланди залишилися важливим імпортером.

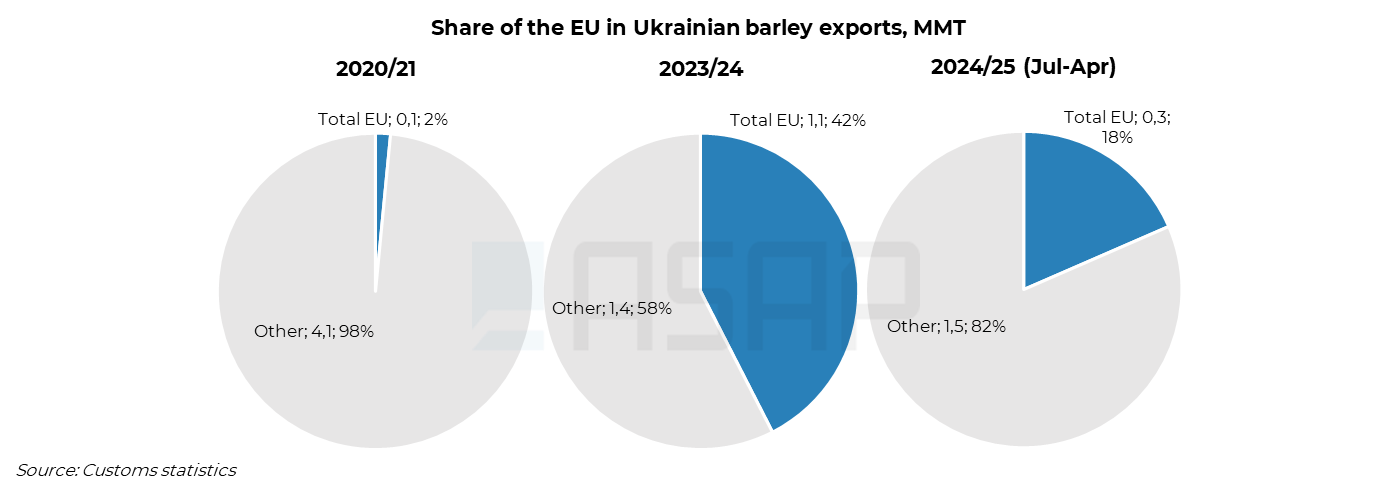

Сегмент ячменю розвивався

схожим чином. У 2020/21 МР частка ЄС в експорті українського ячменю становила

лише 2% (0,1 млн тонн). У 2023/24 МР ця частка зросла до 42% (1,1 млн тонн).

І тут Іспанія закріпила свої

позиції — з нульового імпорту у 2020/21 МР вона вийшла майже на 0,5 млн тонн у

2024/25 МР, ставши другим найбільшим покупцем після Китаю. Також суттєве

зростання імпорту українського ячменю продемонстрував Кіпр.

Зернова дипломатія в дії: пшеничні квоти на горизонті, кукурудза поки поза загрозою

Хоча переговори між Україною та ЄС тривають, за словами джерел, знайомих із ситуацією, перспективи для експорту української кукурудзи до ЄС наразі залишаються відносно позитивними.

Натомість ситуація з експортом пшениці виглядає складнішою. У Брюсселі триває обговорення можливого відновлення квоти на імпорт української пшениці обсягом 1 млн тонн на рік. Обсяги понад цю межу можуть — у певних сценаріях — обкладатися митом у 95 EUR/т. Хоча остаточного рішення ще не ухвалено, у разі його реалізації це може мати суттєвий вплив на експорт української пшениці до ЄС, частка якого у липні-квітні 2024/25 МР становила 35% від загального обсягу експорту пшениці.

Коментар щодо потенційного впливу на іспанську кормову галузь — найбільшого споживача фуражної пшениці в ЄС — надав Хорхе де Саха, генеральний директор Федерації виробників кормів Іспанії:

«Ми не радіємо жодним подіям, які можуть вплинути на ціну чи доступність сировини, яку ми імпортуємо для забезпечення наших потреб. Зараз ми працюємо з нашими органами влади: з одного боку — щоб зберегти прийнятну ціну на імпорт кукурудзи зі США на тлі обговорення мит, з іншого — щоб відкрити ринок ЄС для аргентинської кукурудзи. Це час змін, які можуть переформатувати товарні потоки й ринки на роки вперед. Сподіваємося, що ці зміни зрештою принесуть позитив.»

Його слова відображають ширші занепокоєння європейських імпортерів щодо можливих збоїв у сформованих ланцюгах постачання — зокрема фуражної пшениці — та нагальну потребу у диверсифікованих, стабільних і конкурентоспроможних джерелах.

ASAP Agri продовжить уважно стежити за розвитком ситуації та оперативно

інформуватиме про неї у своїх Преміум звітах.

Повний аналіз доступний для підписників ASAP Agri https://asapagri.com/products

Пов'язані продукти

Прокоментувати