Вікторія Блажко, Катерина Мудріян

У 2024 році ринок олійних культур нагадував справжній блокбастер — з рекордними досягненнями, несподіваними поворотами та інтригою, що задає тон для 2025 року. У ASAP Agri ми ретельно проаналізували ключові події минулого року та визначили основні тенденції, які впливатимуть на розвиток ринку у найближчій перспективі. Займайте свої місця — наступна глава вже розпочалася!

Акт 1: Злети та падіння цін на олійні культури

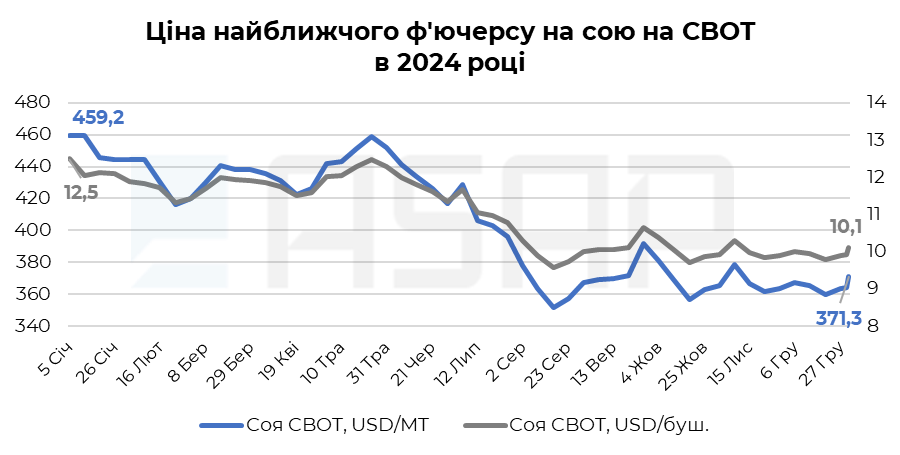

Соя

Ф’ючерси на сою на Чиказькій біржі (CBOT) у 2024 році втратили понад 20% своєї вартості, попри обнадійливий старт. Почавши рік із рівня понад 12 USD/буш., ринок швидко змінив напрямок, коли ведмежі фактори взяли верх. Рекордні врожаї в США та Бразилії у поєднанні зі слабким попитом з боку Китаю спричинили різкий обвал цін. До середини серпня котирування на сою в США опустилися нижче 10 USD/буш., досягнувши найнижчого рівня за останні чотири роки. Спекулятивні продажі ще більше посилили низхідний тренд, додаючи драматизму цьому сценарію.

Проте в жовтні сюжет отримав несподіваний поворот. Зростання імпорту з боку Китаю, закриття коротких позицій спекулянтами та погодні ризики в Південній Америці сприяли підйому цін із мінімальних рівнів. Однак до кінця року котирування сої залишилися переважно нижче 10 USD/буш. під тиском перспектив рекордного врожаю в Південній Америці та невизначеності торговельної політики, яка продовжувала створювати напругу на ринку.

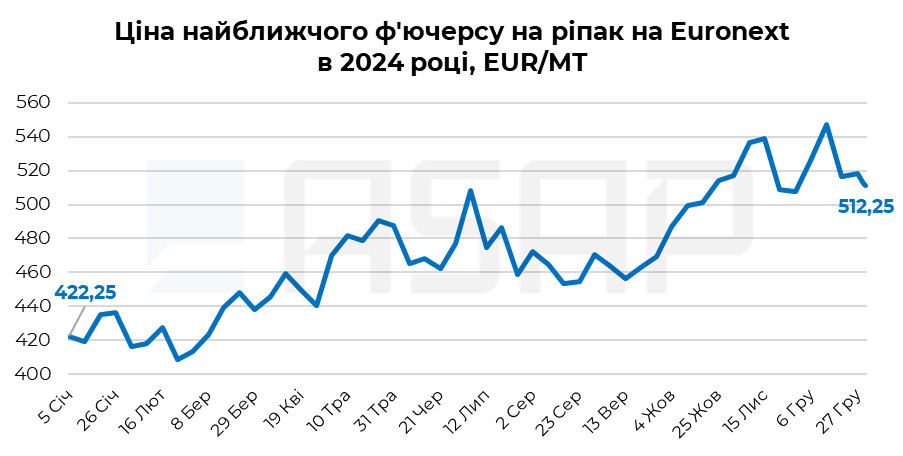

Ріпак

Ф’ючерси на ріпак на Euronext у 2024 році зросли на 20%, перетворивши непростий початок року на впевнене відновлення. У лютому ціни впали до 407 EUR/т через надлишкову пропозицію, жорстку конкуренцію з іншими олійними культурами та слабкий попит на біодизель у Європі.

Однак уже з березня ринок почав відновлюватися. Побоювання щодо врожайності ріпаку стали стимулом для зростання, і до липня ціни перевищили позначку в 500 EUR/т. Прихід нового врожаю тимчасово стримав подальше зростання, але вже у вересні ціни знову повернулися до висхідного тренду. Фінальний акорд року приніс сплеск волатильності, однак ринок зміг утриматися а стабільному рівні, завершивши 2024 рік із цінами вище 500 EUR/т.

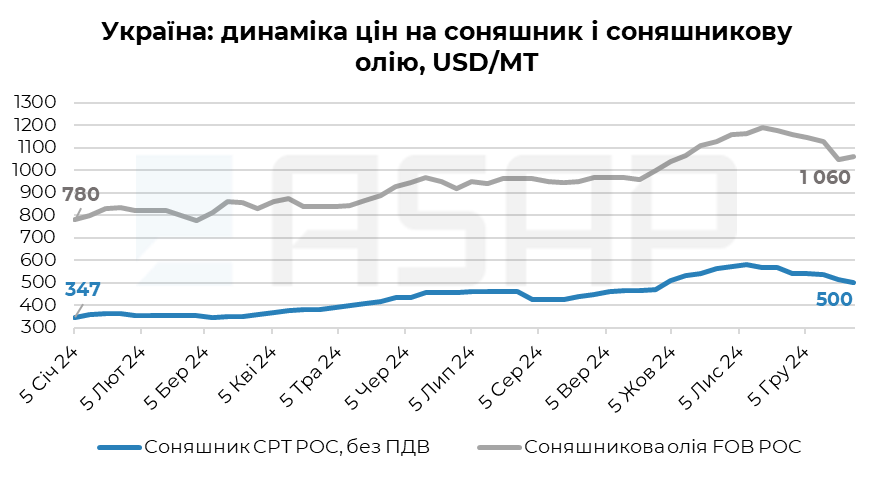

Соняшник

Ринок соняшнику розпочав 2024 рік обережно. У першій половині року ціни CPT в Україні коливалися в діапазоні 340–460 USD/т. Проте в міру того, як історія розгорталася, зменшення виробництва через несприятливі погодні умови та високий попит з боку переробників у Чорноморському регіоні та Європі спричинили стрімке зростання цін. В листопаді ціни CPT POC в перевищили 580 USD/т, перетворивши соняшник на одного із маркет-мейкерів року.

Проте наприкінці 2024-го ринок почав слабшати через негативні маржі переробки та зниження попиту на соняшникову олію. Конкуренція останньої з дешевшою соєвою та пальмовою оліями лише посилила цей тиск, спричинивши корекцію цін. Проте, враховуючи очікуване скорочення пропозиції насіння соняшника в першій половині 2025 року, ця історія ще далека від завершення.

Act 2: Ключові події ринку олійних у 2024 році

Бразилія фіксує рекордний сезон для сої

Якби 2024 рік мав головного героя, це безсумнівно була б соєва промисловість Бразилії. З рекордним виробництвом у 153 млн тонн та експортом, який досяг історичного максимуму в 104,2 млн тонн, Бразилія впевнено домінувала на світовій арені в 2023/24 МР. Стійкий попит з боку Китаю, що закупив понад 70% імпортної сої з Бразилії, закріпив її позиції як беззаперечного лідера у світовій торгівлі соєю.

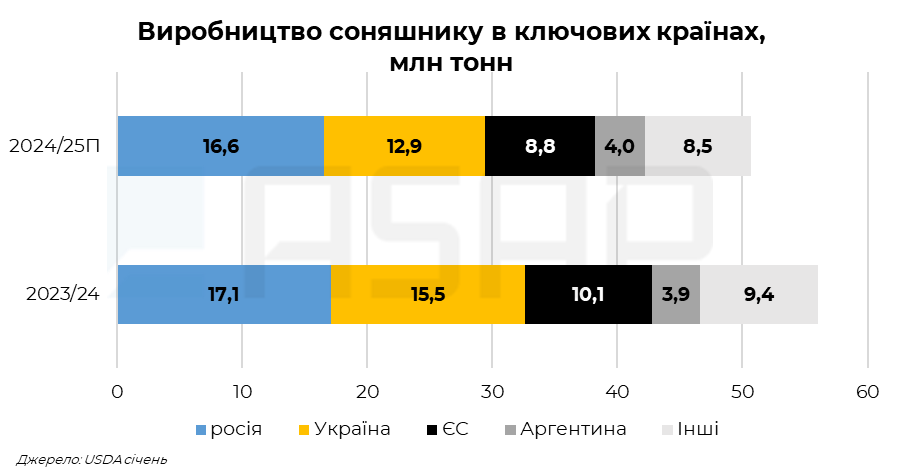

Блискучий сезон для соняшникового комплексу України затьмарюють нові виклики

Україна зміцнила свої позиції як світовий лідер на ринку продуктів переробки соняшнику, експортувавши 4,7 млн тонн соняшникового шроту та 6,3 млн тонн соняшникової олії у сезоні 2023/24. Це був момент тріумфу, який продемонстрував здатність України працювати навіть за складних умов.

Незважаючи на видатні результати України в переробці та експорті у 2023/24 МР, зменшення пропозиції сировини у 2024 році створило серйозні виклики для 2024/25 МР. Виробництво соняшнику в Україні, Росії та ЄС скоротилося на 5 млн тонн. Це суттєве зниження призвело до найбільш напруженого глобального балансу з 2010/11 МР, поставивши переробників та експортерів перед серйозними викликами. Україна виявилася в центрі цієї драми: несприятливі погодні умови скоротили її врожай на 2,5 млн тонн, поглибивши проблеми із забезпеченням ринку. Зменшення пропозиції посилило тиск на переробників, змусивши заводи готуватися до складних рішень і непередбачуваних перспектив.

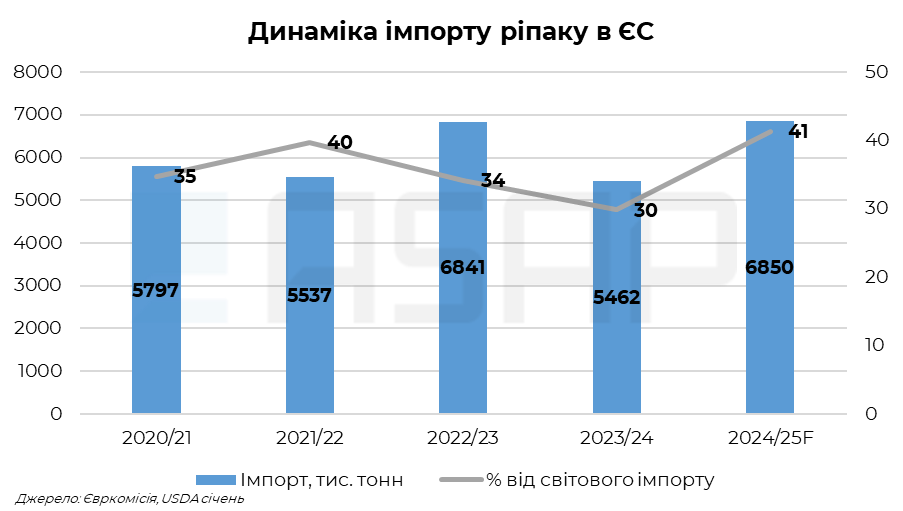

ЄС посилює залежність від імпорту ріпаку

У 2024/25 МР залежність ЄС від імпорту ріпаку повернулася до рекордних показників — обсяги імпорту прогнозуються на рівні майже 6,9 млн тонн. Скорочення внутрішнього виробництва змусило ЄС значною мірою покладатися на постачальників, таких як Канада та Україна, для покриття дефіциту.

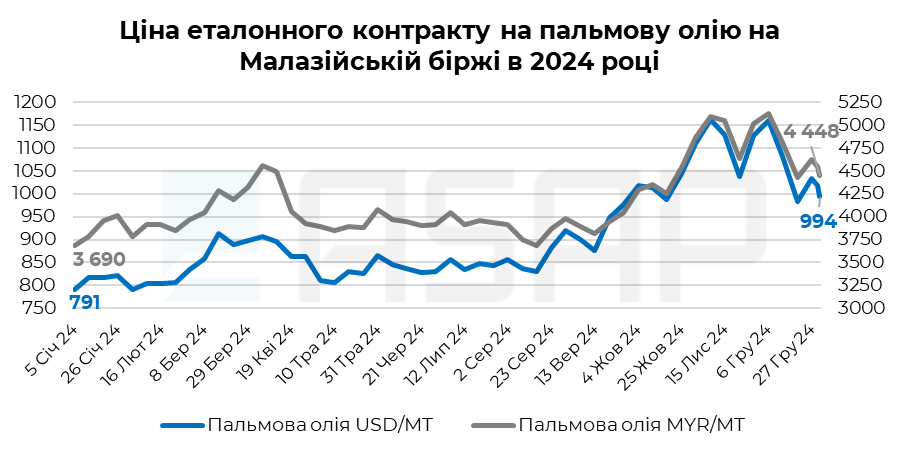

Пальмова олія стає трендсеттером 2024 року

Ф’ючерси на пальмову олію в Малайзії зросли на 25%, досягнувши максимуму в 5 195 MYR/т у листопаді — найвищого рівня з червня 2022 року. Наприкінці року, після різкого підйому, ціни скорегувалися до 4 400–4 620 MYR/т.

Дефіцит пропозиції, спричинений старінням плантацій, нестабільними погодними умовами та обмеженими можливостями для розширення виробництва, підтримував напруженість на ринку. Ще більшого тиску додали новини про впровадження в Індонезії мандату на біодизель B40 з 1 січня 2025 року. Це спровокувало активну закупівлю пальмової олії імпортерами, які побоювалися можливих експортних обмежень. У підсумку, пальмова олія у 2024 році не лише втримала лідерство, але й зміцнила свою роль як ключового регулятора цінових тенденцій на ринку рослинних олій.

Act 3: Чого очікувати у 2025 році?

Погода

У 2025 році погода знову виходить на авансцену, стаючи одним із ключових факторів, що впливають на динаміку ринку олійних культур. У Чорноморському регіоні зима залишається непередбачуваною, і ризики загибелі озимих культур, зокрема ріпаку, продовжують тримати операторів у напрузі. Проте початок року видався спокійним: помірні температури забезпечили стабільний старт без суттєвих втрат. Південна Америка обіцяє більш динамічний розвиток подій.

Олів’є Буйє, керівник відділу продажів KMR Agro та відділу інсайтів та аналітики ASAP Agri

"Наразі ми прогнозуємо рекордний врожай сої цієї весни як у Бразилії, так і в Аргентині," — зазначає Олів’є Буйє, керівник відділу продажів KMR Agro та відділу інсайтів та аналітики ASAP Agri. "Попри те, що ринок частково врахував цей фактор, його справжній вплив залишається недооціненим. Зважаючи на те, що погодні умови продовжують відігравати вирішальну роль, цей сюжет і надалі залишатиметься в центрі уваги ринку аж до завершення збору врожаю”.

Навала сої: рекордна пропозиція у 2025 році

2025 рік обіцяє стати роком нової рекордної пропозиції сої на світових ринках. Бразилія готується зібрати майже рекордний врожай у 170 млн тонн, що стане можливим завдяки розширенню посівних площ та сприятливим погодним умовам, особливо в південних регіонах країни. Доповнює цю картину Аргентина, яка, за прогнозами, додасть ще 52 млн тонн.

Попит на біопаливо

У 2025 році попит на біопаливо приносить нові виклики, які можуть значно вплинути на розвиток ринку. У США законопроєкт, що передбачає цілорічний продаж бензину з вмістом E15, може змінити баланс стимулів на користь етанолу. Це, у свою чергу, створює ризик для соєвої олії — ключової сировини для виробництва біодизеля, яка в нових умовах може опинитися у менш вигідному становищі. Тим часом індонезійський мандат B40, що передбачає збільшення частки біодизеля у паливній суміші з 35% до 40%, обіцяє суттєво змінити динаміку ринку пальмової олії.

Регламент ЄС щодо вирубки лісів

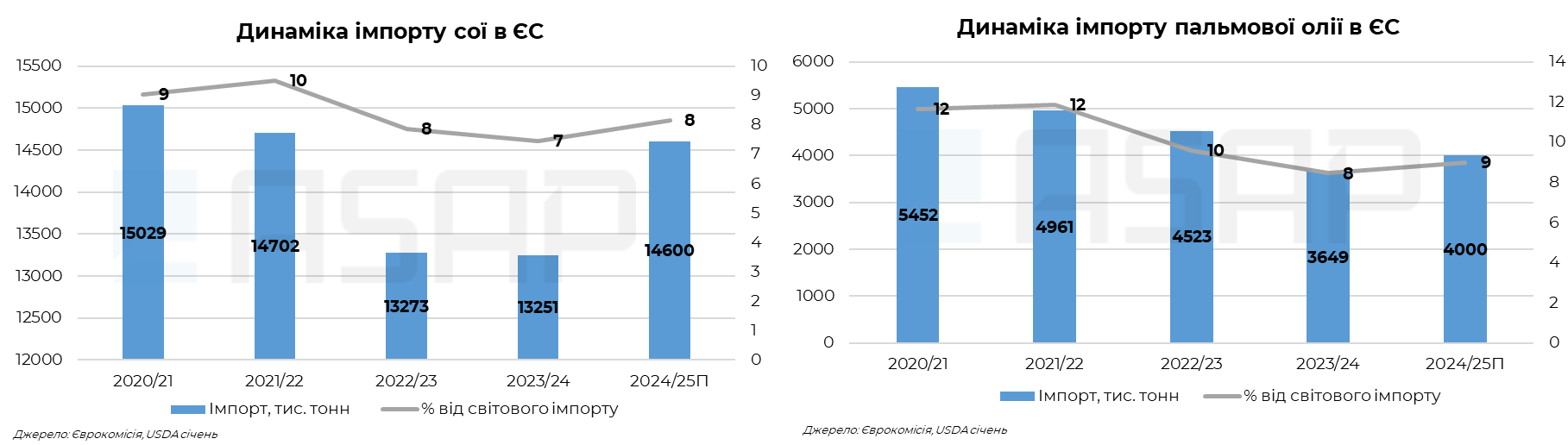

Регламент ЄС щодо боротьби з вирубкою лісів, який набрав чинності 29 червня 2023 року, став справжньою точкою перелому для глобального ринку олійних культур. Відтермінування його застосування до 30 грудня 2025 року дало виробникам цінний час для адаптації, але нові вимоги неминуче матимуть значний вплив на торгівельні потоки та загальну динаміку ринку у найближчі роки. Попри зниження обсягів закупівель в останні роки, ЄС усе ще займає близько 8-9% у світовому імпорті сої та пальмової олії, що підкреслює його вагомий вплив на ці ринки.

Геополітична напруга: торгівля на тонкій кризі

Геополітична напруга у 2025 році обіцяє внести драматичний поворот у сценарій ринку олійних культур, поставивши торговельну політику в центр уваги. Запропоновані президентом США Дональдом Трампом 60% мита на імпорт китайських товарів викликали серйозні побоювання щодо можливих відповідних дій з боку Китаю, які можуть ще більше скоротити експорт американської сої до їхнього ключового покупця.

Український сектор переробки: нова зірка на горизонті

Сектор переробки в Україні готується до змін у 2025 році, переглядаючи свої пріоритети. Наприкінці 2024 року експорт соєвої олії досяг рекордних показників, оскільки багато переробників почали переходити з насіння соняшника на сою, щоб уникнути збиткових марж. Очікується, що ця тенденція лише посилиться в 2025 році, оскільки обмежена доступність насіння соняшника змушує заводи шукати альтернативи та збільшувати обсяги переробки сої.

"Упродовж маркетингового року 2024/25 соя набула для українських переробників такого ж стратегічного значення, як і ріпак минулого сезону. Важливим досягненням стало те, що в грудні 2024 року Україна вперше в історії експортувала 27,5 тис. тонн соєвого шроту судном хендисайз до Іспанії." – Христина Серебрякова, CEO ASAP Agri та брокер Atria Brokers.

Повний аналіз, включаючи матрицю торгівлі соняшниковою олією, доступний виключно передплатникам ASAP Premium.

Пов'язані продукти

Прокоментувати