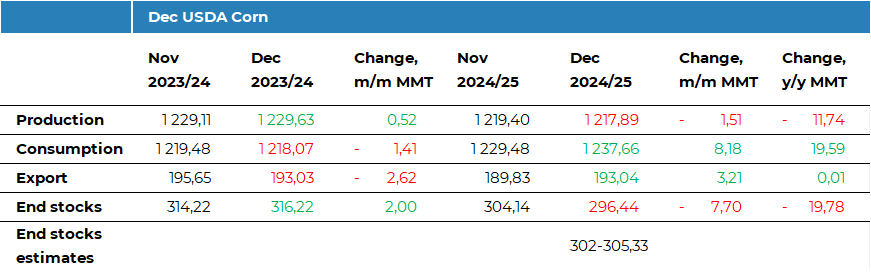

Грудневий звіт WASDE приніс лише кілька

змін у світовому балансі кукурудзи, але ці корективи були суттєвими. Основні

зміни торкнулися США, де прогноз експорту кукурудзи на 2024/25 МР було

підвищено на 3,8 млн тонн до 62,9 млн тонн, а також збільшено прогноз використання

кукурудзи для виробництва етанолу. Це призвело до скорочення запасів на 5,1 млн

тонн до 44,2 млн тонн, що є нижчим за очікування ринку.

Загалом глобальний експорт кукурудзи на

2024/25 МР був підвищений на 3,2 млн тонн до 193,0 млн тонн, без змін для інших

основних експортерів. Глобальне споживання кукурудзи було збільшено на значні

8,2 млн тонн до 1,24 млрд тонн, головним чином завдяки перегляду оцінок для

Бразилії, США, Бангладешу, Ірану та України. У результаті запаси були знижені

на 7,7 млн тонн до 296,4 млн тонн, що значно нижче за очікування.

Тим часом прогноз імпорту кукурудзи в Китай

був знижений ще на 2 млн тонн і тепер становить лише 14 млн тонн.

Що стосується світового виробництва

кукурудзи на 2024/25 МР, то воно було скорочене на 1,5 млн тонн до 1,22 млрд

тонн, зокрема через зменшення прогнозу для ЄС, Мексики та Індонезії, які

частково компенсувалися підвищенням прогнозу для України на 0,3 млн тонн до

26,5 млн тонн.

Звіт надав підтримку цінам, оскільки значне

збільшення глобального попиту та зниження запасів сприяли росту котирувань кукурудзи на CBOT. Однак значне скорочення імпорту для Китаю додає тиску на ринок.

Пов'язані продукти

Прокоментувати