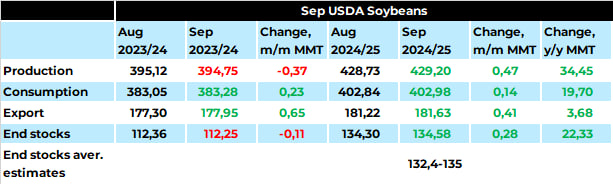

Світовий баланс

попиту і пропозиції сої у вересневому звіті WASDE показав незначні зміни, проте

вищі прогнози експорту та споживання підтримали ціни.

WASDE прогнозує світовий експорт сої в 2024/25 МР на рівні 181,6 млн тонн (+0,4

млн тонн м/м), з єдиним переглядом для Парагваю – на 0,5 млн тонн, до 7,3 млн

тонн. Прогнози для США та Бразилії залишилися без змін – 50,3 млн тонн та 105

млн тонн відповідно.

Світове внутрішнє

споживання прогнозується вище на 0,1 млн тонн, до 402,9 млн тонн, як і імпорт –

на 0,46 млн тонн більше, до 177,7 млн тонн.

Вересневий звіт

WASDE прогнозує світове виробництво сої в 2024/25 МР на рівні 129,2 млн тонн

(+0,5 млн тонн), завдяки підвищенню прогнозів для Канади до 7,2 (+0,3) млн тонн

та Парагваю до 11,2 (+0,5) млн тонн. Прогноз для врожаю США залишився

стабільним – 124,8 млн тонн, як і показники врожайності, хоча деякі учасники

ринку очікували змін через суху погоду.

Прогнози врожаю

Бразилії та Аргентини на 2024/25 МР також не змінилися – 51 млн тонн і 169 млн

тонн відповідно.

Запаси сої у новому

сезоні вересневий WASDE оцінює трохи вище – на рівні 134,5 млн тонн (+0,3 млн

тонн), що знаходиться у верхньому діапазоні очікувань ринку. Проте аналітики

знизили прогноз запасів сої у США в 2024/25 МР – на 0,3 млн тонн, до 14,9 млн

тонн, що відповідає середньому прогнозу ринку та підтримує ціни у

короткостроковій перспективі.

Загалом, вересневий

звіт WASDE по сої є досить нейтральним, і в короткостроковій перспективі ціни

будуть більше залежати від розвитку погодних умов у Південній Америці, особливо

у Бразилії, де посуха вже викликає побоювання щодо затримки посіву нового

врожаю. На момент публікації,

ф'ючерси на сою на CBOT зростали, оскільки

торгівля все ще надихається експортними продажами сої зі США минулого тижня.

Пов'язані продукти

Прокоментувати